SK hynix Patent Filing Trends: Analysis Based on the July 6, 2026 Search Snapshot

Pinepat

July 12, 2026

SK hynix's patent portfolio should not be read merely as the filing volume of a memory semiconductor company. The dataset shows manufacturing processes, device structures, memory circuits, storage systems, and the newer H10B memory-device classes appearing together. In practical terms, SK hynix appears to be building both process-level defensive layers and system-level claim coverage.

This column is based on the search and collection snapshot dated July 6, 2026 from pinepat_mhkang_concat_2026_07_06.xlsx. The concat sheet contains 148,463 raw document records. Because one application can appear as multiple publication or grant records, filing-year trends and jurisdiction shares are analyzed mainly on 104,342 deduplicated application records, using jurisdiction code plus application number as the deduplication key.

| Search snapshot | 2026-07-06 |

|---|---|

| Raw document records | 148,463 rows |

| Deduplicated applications | 104,342 records |

| Filing-year coverage | 1985-2026 |

| 2026 data | Partial count as of July 6 |

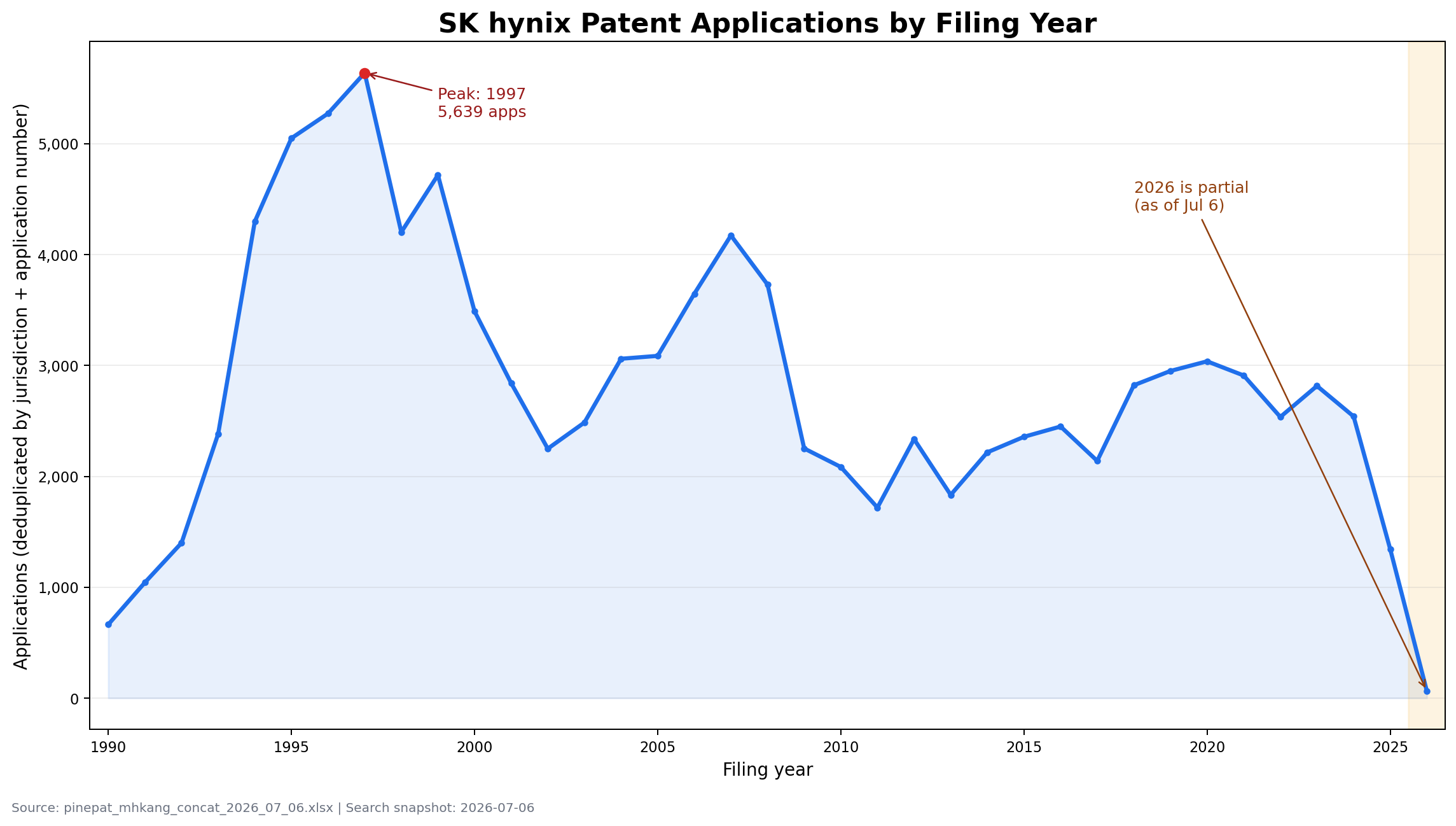

On the deduplicated basis, SK hynix-related filings peak in the mid-to-late 1990s. The highest point is 1997, with 5,639 applications. The 1995-1999 period forms a thick base layer of rights around semiconductor manufacturing processes, memory cells, DRAM structures, and fabrication methods. A second visible wave appears in 2006-2008, where process scaling, gate structures, flash and DRAM fabrication, and memory-circuit control technologies were accumulated together.

Since 2016, annual filings have generally stayed in the mid-2,000 to roughly 3,000 range. The lower numbers for 2025 and 2026 should not be read as a simple decline in research activity. Patent databases lag recent filing activity because many applications are not published immediately after filing. As of the July 6, 2026 search snapshot, the most recent years are therefore an incomplete publication window.

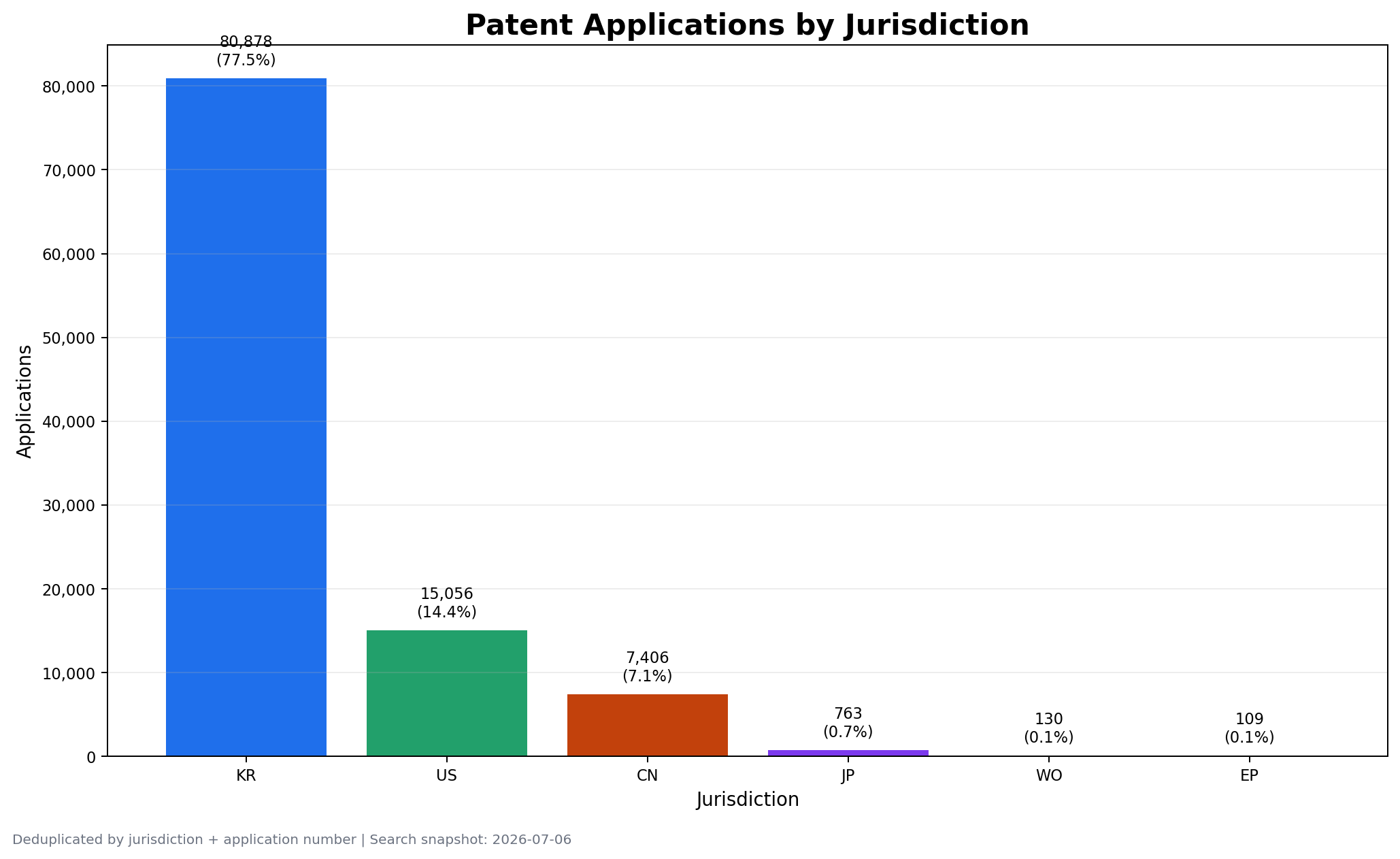

Korea accounts for 80,878 applications, or 77.5% of the deduplicated set. This reflects the company's domestic R&D and manufacturing base and the richness of Korean records in the source data. Outside Korea, the United States has 15,056 applications and China has 7,406. The United States remains central for semiconductor and storage-system licensing, disputes, customer ecosystems, and high-value enforcement. China is increasingly important from manufacturing, sales, and supply-chain perspectives.

Japan, WO, and EP records are smaller in count, but the number alone does not determine importance. In semiconductor portfolios, selective foreign entry may depend on product families, equipment and material collaborations, standards, or customer locations. The more important question is which technology classes were extended into which jurisdictions.

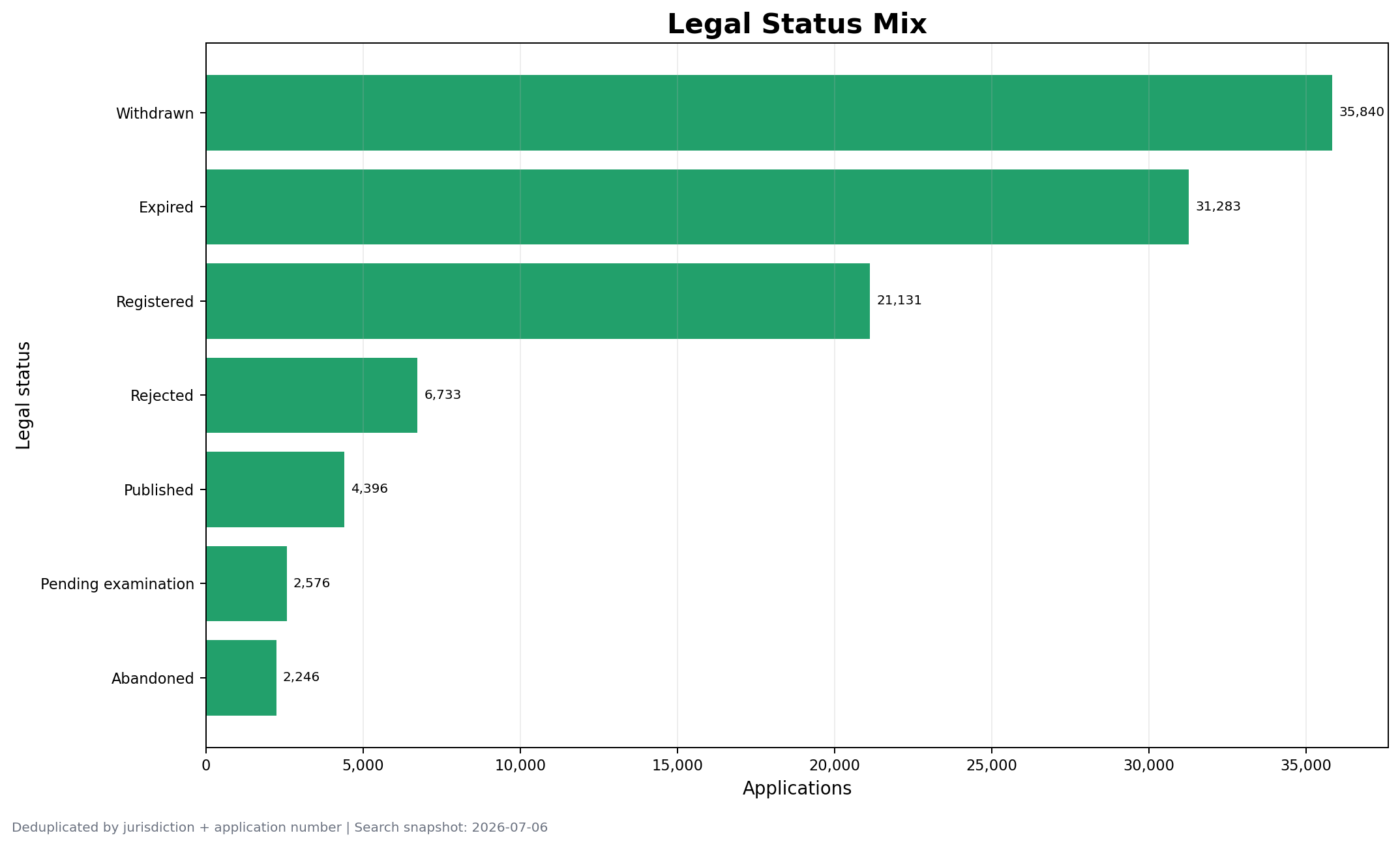

The deduplicated status mix shows 35,840 withdrawn applications, 31,283 expired rights, 21,131 registered rights, 6,733 rejected records, 4,396 published applications, and 2,576 pending cases. A high share of withdrawn or expired records is not automatically a negative signal. Much of the 1990s and early-2000s volume has naturally reached term expiry or has been pruned based on maintenance costs, product relevance, and generation changes.

The remaining registered, published, and pending layer is still meaningful. For technologies tied to current products, such as memory systems, controllers, error correction, 3D memory structures, and storage-management methods, claim scope and foreign family status matter more than raw count.

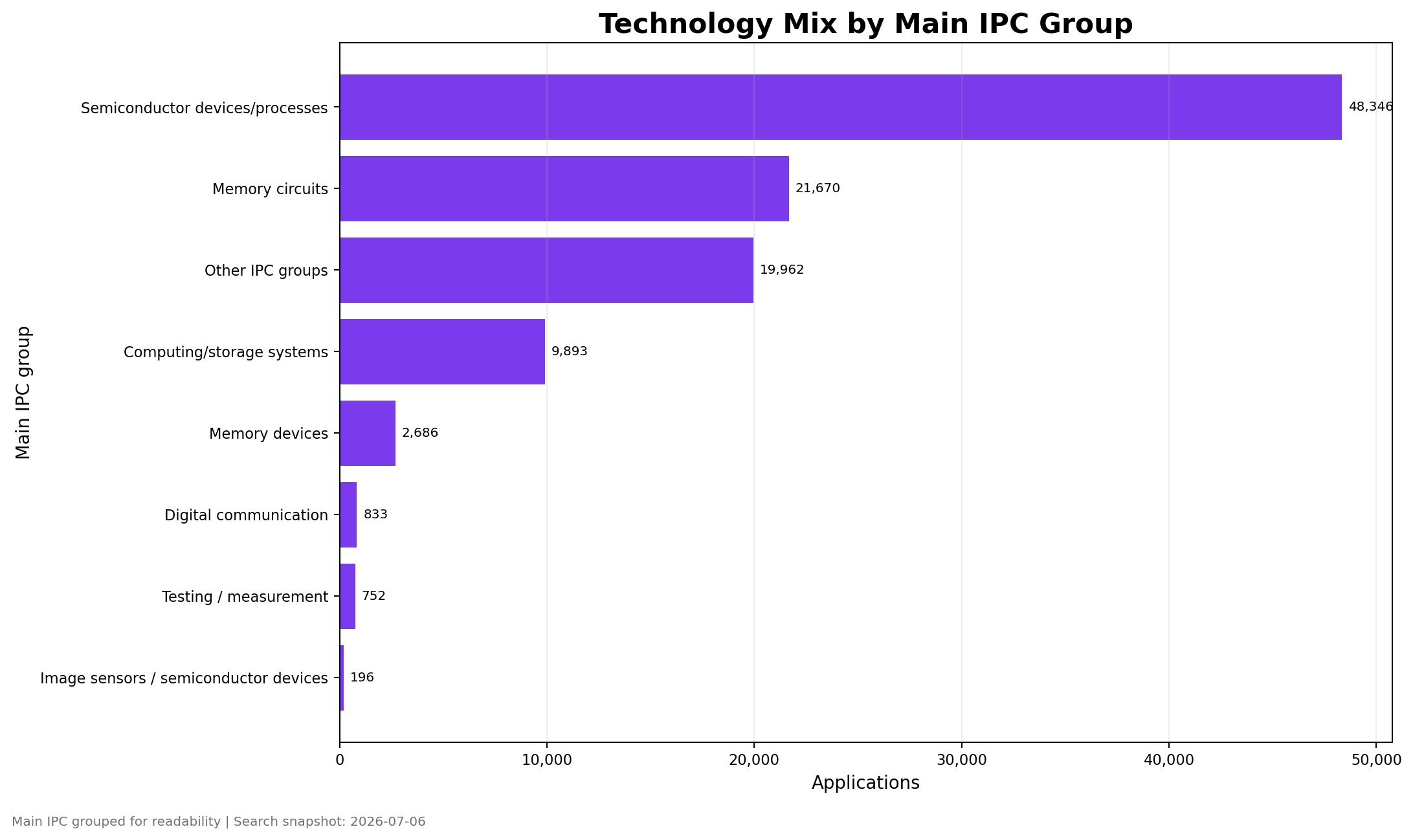

Grouped by main IPC, semiconductor devices and processes under H01L form the largest block, with 48,346 applications. Memory circuits under G11C follow with 21,670 applications, while computing and storage systems under G06F account for 9,893. H10B memory-device classifications add another 2,686. The portfolio therefore extends from wafer processing and cell structures into memory operation, testing, error control, and storage-system architecture.

| Top main IPC 1 | H01L-021/28: 5,563 applications |

|---|---|

| Top main IPC 2 | H01L-021/027: 3,829 applications |

| Top main IPC 3 | G06F-003/06: 3,229 applications |

| Top main IPC 4 | H01L-021/336: 3,181 applications |

| Top main IPC 5 | H01L-027/108: 3,023 applications |

| Top main IPC 6 | H01L-027/115: 2,528 applications |

H01L-021/28, H01L-021/027, and H01L-021/336 point to strong protection around fabrication and structural formation. G06F-003/06, by contrast, can be directly relevant to storage-device I/O, data placement, memory-system control, and product-level freedom-to-operate reviews. For competitor monitoring, H01L alone is not enough; G11C, G06F, and newer H10B classes should be searched together.

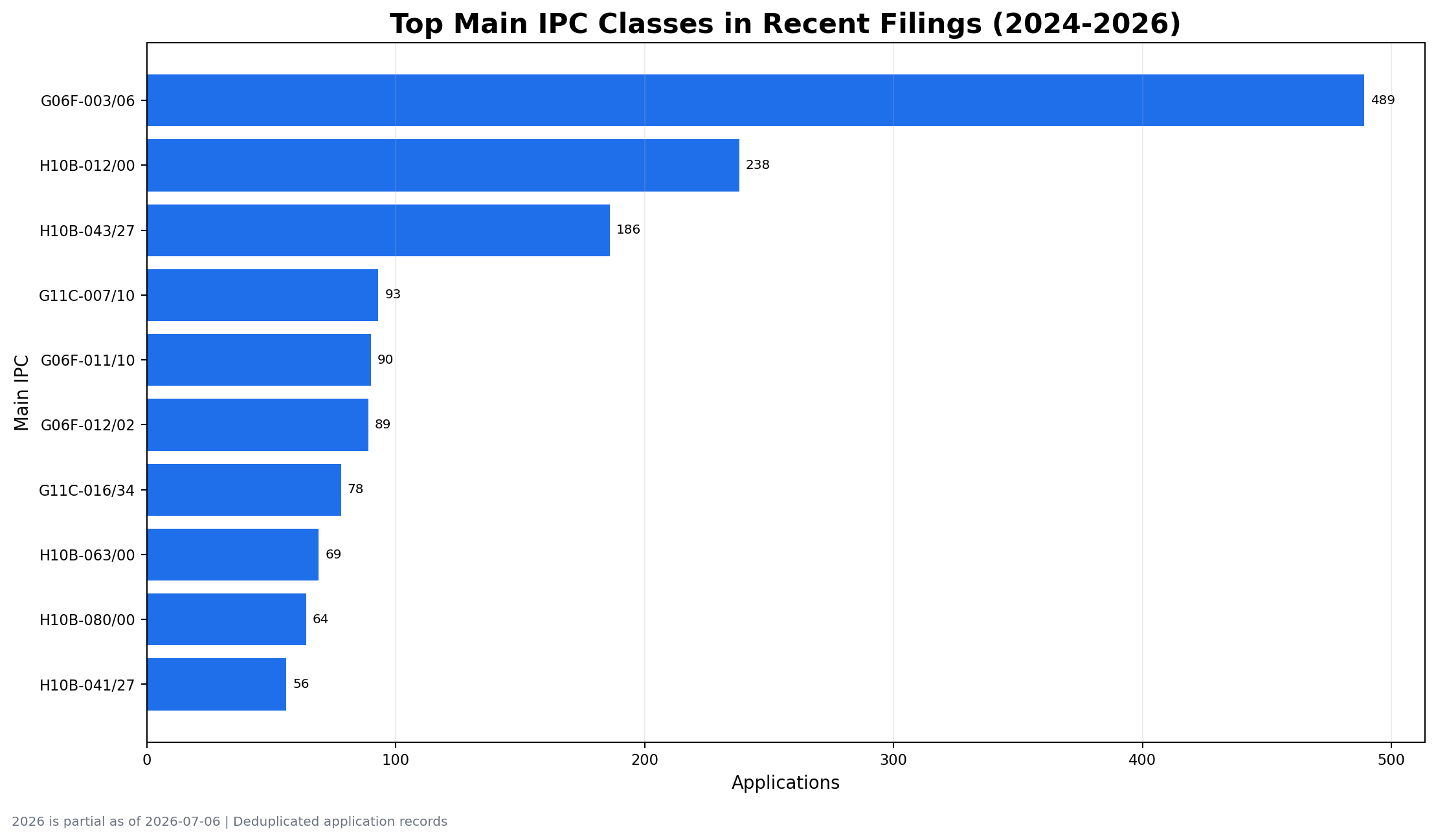

In the 2024-2026 window, G06F-003/06 leads with 489 applications, followed by H10B-012/00 with 238 and H10B-043/27 with 186. G06F-011/10, G06F-012/02, and G11C-016/34 also rank highly. This suggests that recent claim drafting is moving from cell fabrication alone toward storage systems, error correction, data management, and device-structure combinations.

The rise of H10B is also important. It partly reflects IPC classification changes, but it also matches the technical need to classify 3D memory, nonvolatile memory, and detailed memory-device structures more precisely. A search strategy limited to older H01L and G11C expressions can miss relevant recent filings.

Based on the July 6, 2026 search snapshot, SK hynix's patent portfolio combines a thick H01L manufacturing-process base with expanding claim coverage in G11C, G06F, and H10B. The high number of expired and withdrawn records is better understood as a result of technology-generation changes and portfolio pruning, not as a simple weakening of the portfolio. Future monitoring should focus less on raw filing volume and more on recent publications, foreign families, and system/device claims centered on G06F and H10B.