7 Key Factors for Pre-Investment IP Due Diligence

Pine IP Firm

May 12, 2026

Investors do not invest simply because a technology is good. They verify whether the technology belongs to the company, if competitors can easily copy it, if the rights remain with the company even if key personnel leave, and if it infringes on external rights. Intellectual property is the area most frequently examined during this process.

Early-stage startups often mistakenly think that IP due diligence is a procedure only for large corporate M&As. However, even at the seed, pre-A, and Series A stages, investors look for minimal IP risks. Especially for AI, SaaS, healthcare, manufacturing, robotics, semiconductor, battery, content, and platform companies, IP organization can directly affect investment speed and terms.

Before raising investment, the following seven points should be checked first.

The first thing to look at is ownership of rights. It's important to confirm who created the technology and whether those rights have been transferred to the company.

The following situations frequently become issues during due diligence.

Investors first look at “can the company sell this technology?” rather than how excellent the technology is. Therefore, it is advisable to prepare separate assignment agreements or confirmations for developments made before company incorporation, outsourced deliverables, and co-development results.

A large number of patents does not necessarily mean a good portfolio. Investors look at whether patents are connected to the actual business.

Key points to check:

Investors are more curious about “what does this patent mean for revenue and defensive strength?” rather than simply “there are patents.” Therefore, it is advisable to include a mapping table connecting product functions and patent claims in investment materials, rather than just a list of patents.

Even technology companies should not take trademarks lightly. If product names, service names, app names, or platform names are already being used in marketing but trademarks have not been filed, or if similar trademarks already exist, rebranding costs may arise.

Questions examined during due diligence:

Trademarks can become a business risk faster than patents. Brand rights should be organized before significant advertising spending after investment.

For SaaS and AI companies, open-source usage history is central to due diligence. Even if investors do not directly review the entire source code, they can verify the list of open-source components used, licenses, notification obligations, and the use of strong copyleft licenses.

The following, in particular, are high-risk signals:

Before investment, at a minimum, a product-specific open-source list and license classification table should be created.

Not all technologies can be patented. Datasets, recipes, manufacturing conditions, customer-specific tuning values, pricing logic, labeling standards, and experimental failure data may be better managed as trade secrets.

However, trade secrets are not protected merely by thinking they are “secret.” Actual management measures must be in place.

Checklist items:

Investors look not only at how well the company has developed its technology but also whether it has a system in place to prevent losing that technology.

Possessing a patent does not automatically grant the freedom to sell a product. A company's patent is a “right to prevent others from copying,” while FTO (Freedom-to-Operate) is a review to determine “whether we can operate without infringing on others' rights.”

Before investment, the following issues should be checked:

Especially in manufacturing, medical devices, robotics, batteries, semiconductor equipment, telecommunications, and security sectors, FTO review can become crucial in investment due diligence.

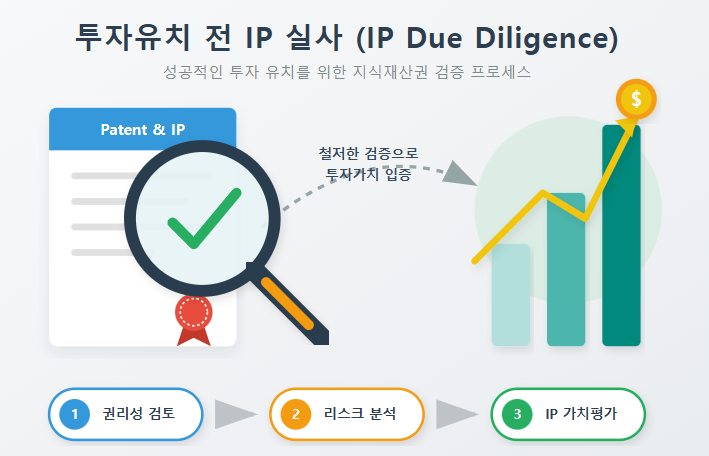

IP can serve as a basis for fundraising and commercialization, not just a cost item. WIPO also explains that intellectual property and intangible assets are becoming more important in corporate fundraising. However, for IP to be used for fundraising, its rights status, business relevance, marketability, feasibility of implementation, and licensing potential must be well-organized.

From an investor's perspective, good IP materials demonstrate the following:

A table connecting products, technology, rights, and markets is far more persuasive than a simple list of patents.

It is advisable to prepare the following documents in folders before investment due diligence.

They do not necessarily have to be registered. However, it is important whether at least an application has been filed for core technologies, whether it was filed before public disclosure, and whether the claims are connected to the product. For early-stage companies, filing timing and the direction of rights are often more important than registration.

It can be disadvantageous for technology companies. However, not all companies need to be patent-centric. Some businesses prioritize data, brands, trade secrets, software copyrights, or contractual exclusive rights. The important thing is to be able to explain “why there are no patents, and what is used for defense instead.”

It is when the ownership of rights is unclear. Core code created by an outsourcing company, patents under a co-founder's personal name, commingling with technology from a previous employer, or unauthorized use of university research results can delay transactions or worsen terms.

Startups preparing for investment should not only look at patent filing status but also organize rights ownership, trade secrets, open source, trademarks, FTO, and contracts. If IP due diligence is rushed just before investment, unfixable problems may emerge.

Pine IP Firm organizes materials that can answer investors' questions through pre-investment IP checks, patent portfolio diagnostics, product-specific rights mapping, and open-source/outsourcing contract risk reviews.